Company Overview

Procore Technologies, the leading cloud-based construction management software provider, filed for a $100M IPO. Per usual, the $100M figure is a placeholder and is likely to rise significantly by the time the company prices their IPO. Goldman Sachs is leading the IPO and Procore plans to trade on the New York Stock Exchange (NYSE) under the ticker “PCOR".

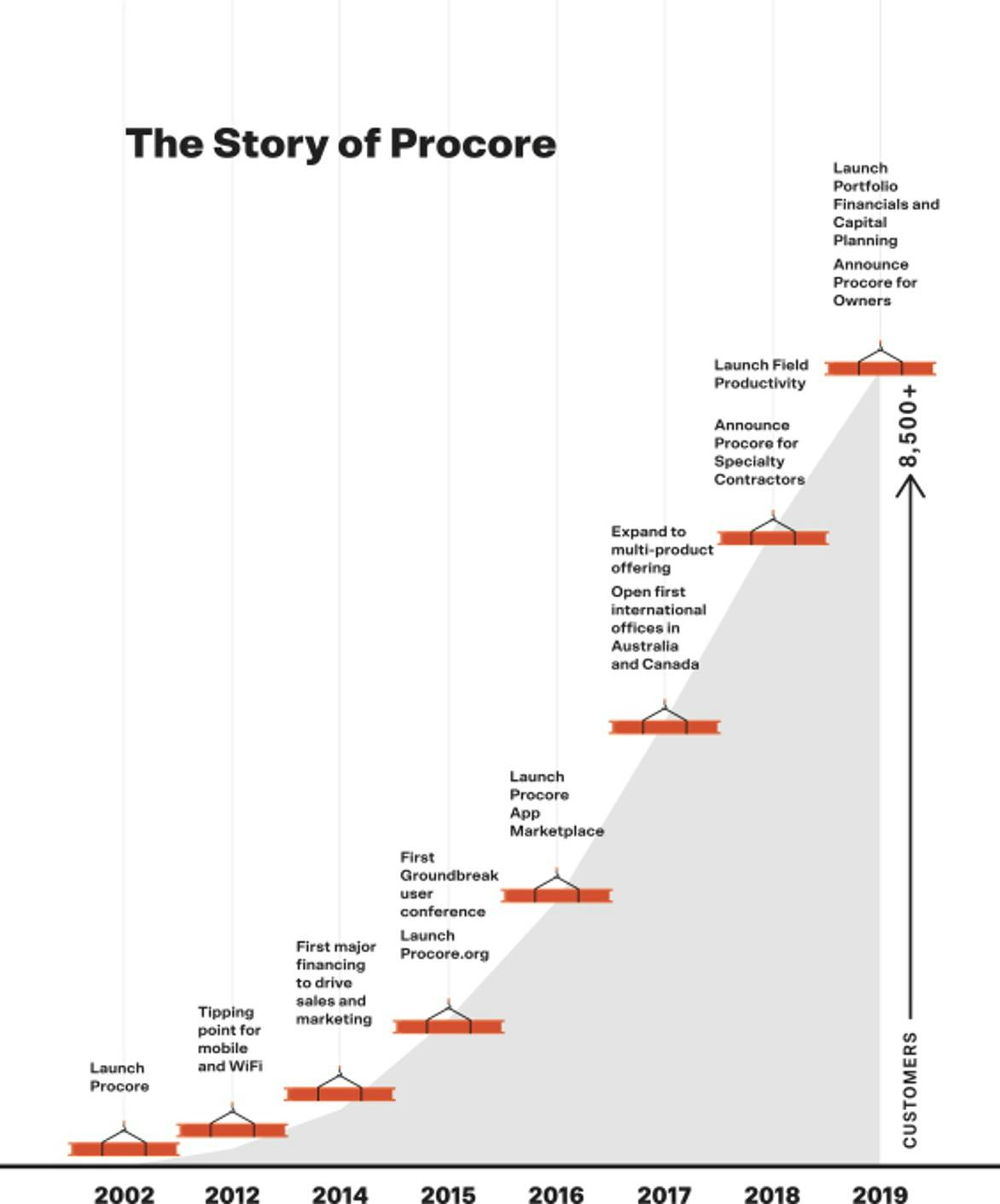

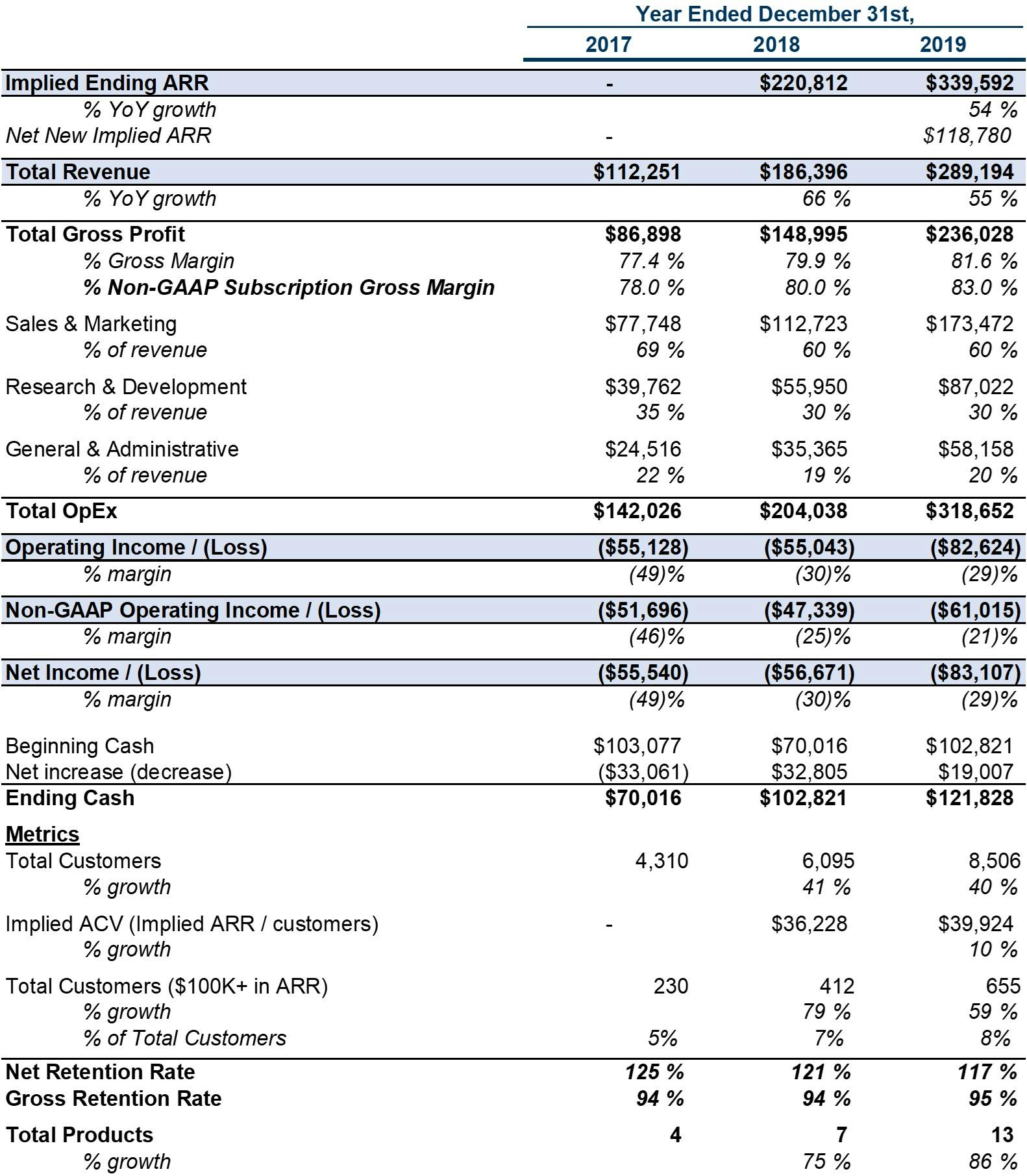

Procore's mission is to "connect everyone in construction on a global platform" and it operates in one of the oldest and least digitized industries in the world -- construction -- which represented ~13% of GDP, and employed 7% of the global workforce in 2017. Most of the industry still relies on pen and paper, email, fax and other on-premise software tools. Craig “Tooey” Courtemanche, Jr., founder and CEO of Procore, started the company in 2002 while facing frustration with his own home construction project. The first product was only accessible online through their website and they saw little market traction until 2012 when they saw advances in WiFi, connectibity and proliferation of smartphones and tablets. The company has also significantly expanded their suite of products both organically and through acquisitions (more below) and today offers an integrated SaaS platform that spans 4 product categories 1) Preconstruction 2) Project Management 3) Resource Management and 4) Financial Management enabling their customers to manage the entire construction lifecycle through their software. While Procore has been around almost two decades, the traction of the business over the past few years has been outstanding. The company did $289.2M in revenue in 2019, up 55% YoY with 8,506 customers running projects in 125+ countries. They ended last quarter at $339.6M of implied ending ARR (quarterly subscription revenue * 4), up 54% YoY. Procore is based in Carpinteria, California (near Santa Barbara) and has 1,911 full-time employees. The company was incorporated as Butterfly Lane, Inc. in January 2002, and changed their name to Procore Technologies, Inc. in May 2002.

Company timeline graphic:

Source: Company S-1

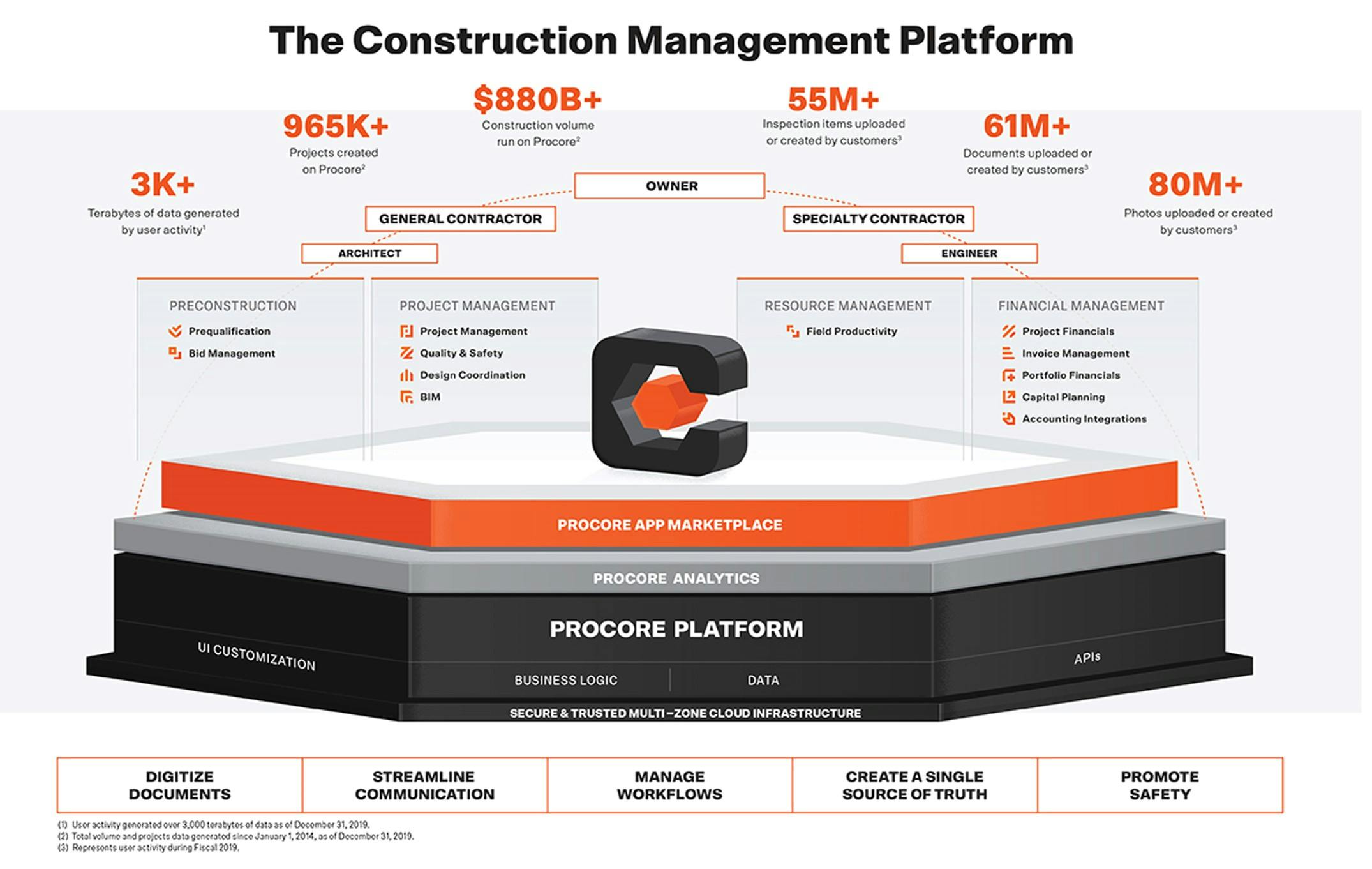

Product

Source: Company S-1

Procore's products span the construction lifecycle for their customers and includes bidding, scheduling, labor tracking, financial management, building information modeling and also offers open APIs and the Procore App Marketplace, which enables customers to integrate the Procore product with their internal systems and 180+ 3rd party applications for accounting, document management, scheduling and more. The App Marketplace has been widely adopted by customers and ~72% of customers have at least 1 integration and 40%+ have two or more. The company's platform streamlines communication and facilitates compliance with safety & regulatory standards, increases efficiency & reduces rework and delays, improves safety, and enhances collaboration and accountability among key stakeholders. Procore has been successful in building (or buying) new products and as of 31-Dec-2019, 59% of their customers subscribed to 3 or more of their products (41% have 4+ products), of which they have 13 in total. This enables the company to have strong upsell characteristics (more on retention later). Across their 8,500+ customers, the company had 1.3 million users in 2019, which they define as their customers' employees. 60% of which are "collaborators", which are users involved in a project but don't have control over what data they can access and more limited functionality. Moreover, customers can invite all project participants to engage with the platform as part of a project team. In 2019, on average each customer invited 170+ project participants. The company designed their products for owners, general contractors, and specialty contractors. Procore's product is run on AWS. More on their main product categories and descriptions below:

Preconstruction: Procore's Preconstruction products facilitate collaboration between internal and external stakeholders during the planning, budgeting, and partner selection phase of a construction project.

Project Management: The Procore Project Management products connect entire construction project teams by ensuring project information is aggregated in a cloud-based platform, available to all project participants, and accurate so that work on the jobsite is completed correctly. They also enable enable real-time collaboration, information storage, design, and regulation compliance.

Resource Management: Their Resource Management product helps customers track labor productivity and manage profitability on construction projects.

Financial Management: Procore's Financial Management products provide customers with visibility into the financial health of their individual construction projects and portfolios and facilitate access to financial data, linking the field and the office in real-time.

Procore also offers Procore Analytics, which is a business intelligence product to improve their customers' decision-making processes. It has ~100 pre-built reports and was launched in the fall of 2019. Procore ends up becoming the system of record for customers' construction projects and as of the end of 2019, Procore's user activity generated 3,000+ terabytes of data and in 2019 on average added 110+ terabytes of data per month.

Procore mentions some ROI statistics for their customers and according to the 2018 Procore Survey, 93% of individual respondents say their company is more protected against claims or litigation due to the data tracked in Procore. A few more stats from the 2018 Procore survey below:

87% of individual respondents reported that after using Procore's products, submittals were processed faster.

84% of individual respondents reported they were able to process requests for information, or RFIs, faster.

85% of individual respondents reported closing punch list items faster after using Procore's products.

90% of individual respondents said their client satisfaction has increased since using Procore.

Summary Metrics and GTM (Go-to-Market)

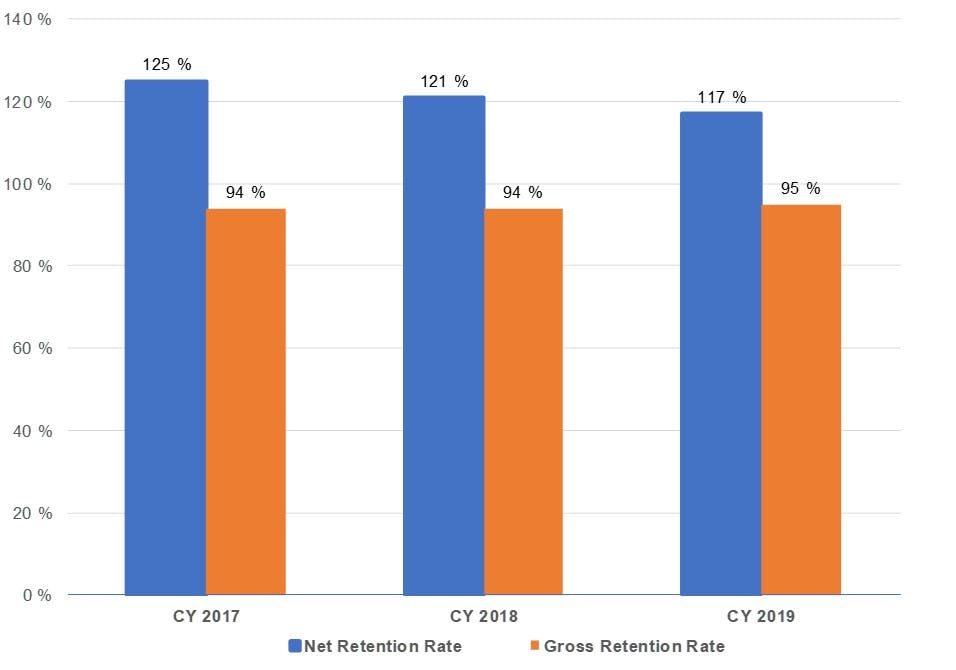

Procore's revenue is substantially all subscription in nature and offers an unlimited user model designed to facilitate maximum usage by project stakeholders. They do not charge on a per-seat-basis but charge fixed fee subscriptions depending on the number and mix of products, along with the annual construction volume contracted through the system. Subscriptions are generally annual or multi-year and customers range from small businesses doing a few million of annual construction volume to global enterprises managing billions of dollars of annual construction volume. Procore targets owners, general contractors, and specialty contractors as customers across commercial, residential, industrial, and infrastructure segments. Procore sells through a direct sales team which is segmented based on customer size. They utilize an inside sales model for smaller customers and a field sales team for large accounts. Procore did $289.2M in revenue in 2019 and grew 55% YoY and had a (21)% non-GAAP operating margin in the same year. Their operating margins have been improving steadily over the past 3 years. Taking implied ending divided by total customers, the average customer paid ~$40K in 2019. Across their 8,500+ customers Procore had a 117% net dollar retention rate and 95% gross dollar retention rate. Customers that are $100K+ in ARR are growing almost 60% YoY and represent 8% of total customers. Below are more stats on the business as well as industry stats from the S-1:

Procore customers rely on their platform to help run their businesses as evidenced by the fact they have used the platform to create an aggregate of 965,000 projects representing over $880B of construction volume since 1-Jan-14, with over 370,000 projects created in 2019 alone.

In 2019, the average duration of an active project in Procore was ~20 months.

In 2019, 63% of the growth in revenue was attributable to revenue from existing customers and 37% was attributable to revenue from new customers.

Procore has grown their product offerings 3x+ from 4 in 2017 to 13 today.

Someone earns a Procore certification on average every 4 minutes and the company has issued over 200,000 certifications to date. In addition, 86% of accredited U.S. construction management programs teach students about the Procore platform.

In 2019, Procore customers uploaded or created 80+ million photos, 61+ million documents, and 55+ million inspection items.

In 2019, the average Procore support response time to a user support request via online chat or phone was under 60 seconds, and they had a positive customer support satisfaction rating of over 90%.

Customers are running projects in 125+ countries, and 11.3% of revenue in 2019 was generated from customers outside the United States.

Sales commissions are amortized on a straight-line basis over the expected period of benefit, which is 4 years for Procore.

Most new customers come in the 4th quarter of each year.

Procore has 2 issued patents, 17 pending patent applications in the United States, and 3 Patent Cooperation Treaty international patent applications.

Industry Stats

According to a 2018 JBKnowledge construction survey, ~93% of construction workers surveyed use a smartphone and 62% use a tablet every day.

According to a Deloitte report, the construction industry spends half as much on IT compared to the average across all industries. And while IT spend is lower, 80% of contractors surveyed in a USG Corporation and U.S. Chamber of Commerce survey believe that they will use some newer technology by 2022.

Annual worldwide construction spend, which consists of new construction and ongoing maintenance and modifications, is expected to grow from ~$10T in 2017 to ~$14T by 2025, according to McKinsey.

The 2018 FMI Report estimates that employees at construction companies spend 35% of their time on “non-optimal” tasks and this cost the U.S. construction industry an estimated $177.5B in labor costs in 2018. According to McKinsey, the typical non-residential construction project runs 80% over budget and 20 months behind schedule.

In 2017, the UN estimated that over the next 40 years, 2.5T square feet of new construction will need to be built globally in order to meet population growth and urbanization expectations. Construction at this rate would be roughly equivalent to building a city the size of New York City every month for the next 40 years.

Market Opportunity

Given the lack of software adoption in the construction industry, there's certainly a large market opportunity for Procore. Procore arrives at a ~$9.2B TAM number based on taking the Gartner estimate of 6.1% for application software spend (against all IT spend across industries) and applying that to the $10T number of total construction revenue estimate from 2017. They also find a ~$9.4B number by applying their median ARR by company size from a report they commissioned that includes an estimate of total addressable customers. Based on that report, Procore believes they're only 2% penetrated among their total addressable customer base. The company also has limited international revenue to date and is another area of opportunity.

Competition

Procore believes they compete against multiple other horizontal and vertical-specific software vendors, as well as in-house tools. Oracle and Autodesk have made significant strides in this market and are likely the most fierce competitors, especially at the higher-end of the market. A summary of those companies and segments are below:

Construction management products offered by Oracle (acquisitions of Primavera Systems, Aconex, and Textura), Autodesk (acquisitions of PlanGrid, Assemble Systems, and BuildingConnected), and Trimble (acquisitions of Viewpoint and e-Builder).

Accounting software vendors including ComputerEase Software, Foundation Software, and Jonas Software.

Point solution vendors selling products in one part of the workflow stack including analytics, bidding, BIM, compliance, and scheduling.

In-house tools or processes.

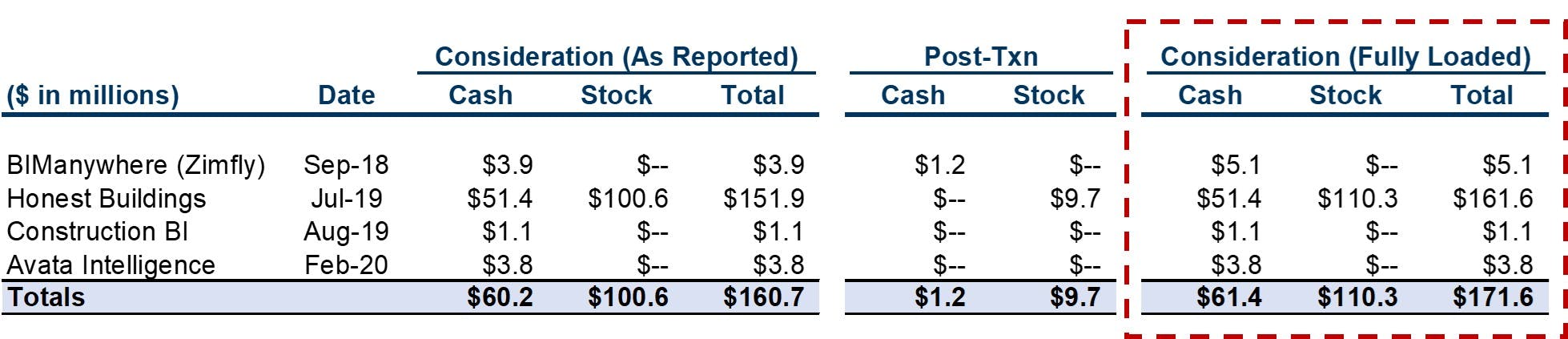

Acquisitions

It's worth nothing that Procore has made a number of acquisitions over the past few years to boost their product suite and has spent $171.6M in cash and stock on 4 companies since 2018. An output of those are below:

Source: Company S-1

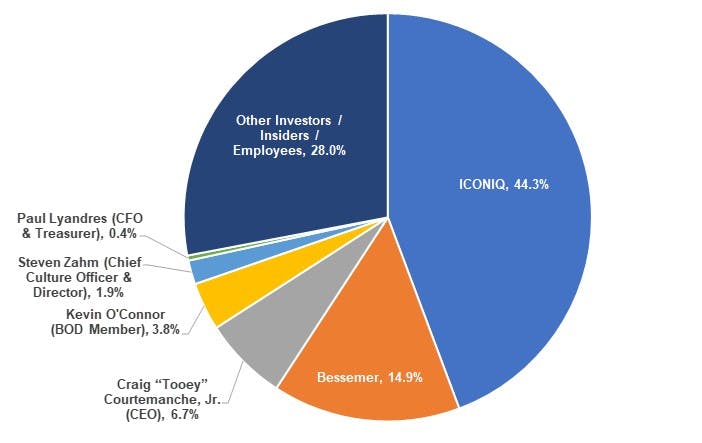

Investors and Ownership

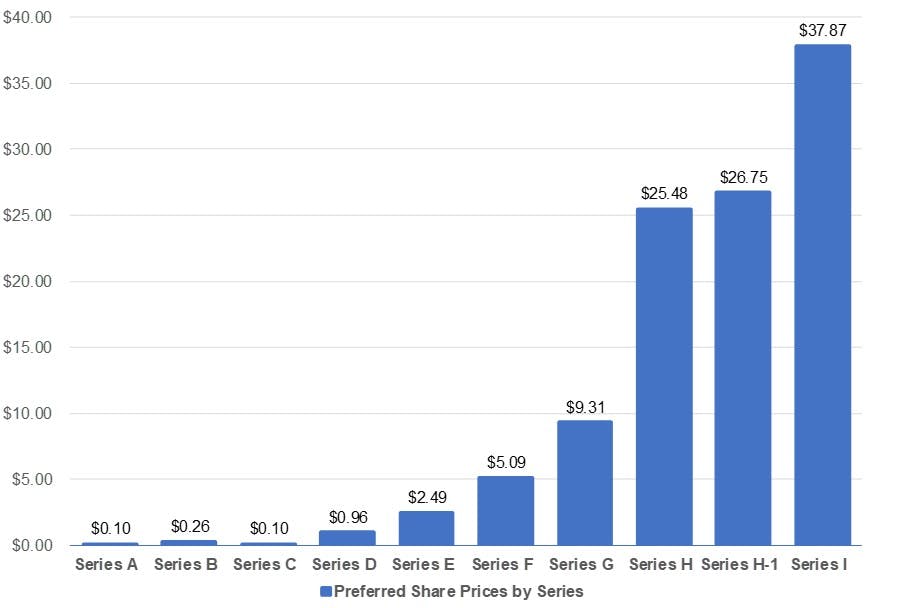

According to Pitchbook, Procore has raised $490M to date from investors including Bessemer, ICONIQ, Dragoneer, Tiger, Lead Edge, Persistence Capital Partners, and others via Series A through I financings. 5%+ pre-offering institutional investor shareholders include ICONIQ (44.3%) and Bessemer (14.9%). CEO and founder, Craig “Tooey” Courtemanche, Jr., is at a 6.7% pre-offering stake. From September 2019 through January 2020, Procore sold 2.5M+ shares of Series I preferred stock at $37.87 a share (~$95M in total). At that share price, the company was valued ~$4B in the private markets.

Outputs of their capitalization table and preferred stock financings are below:

% Ownership, Pre-Offering

Source: Company S-1

Preferred Stock Share Prices by Series

Source: Company S-1

Financials and Other Metrics Outputs

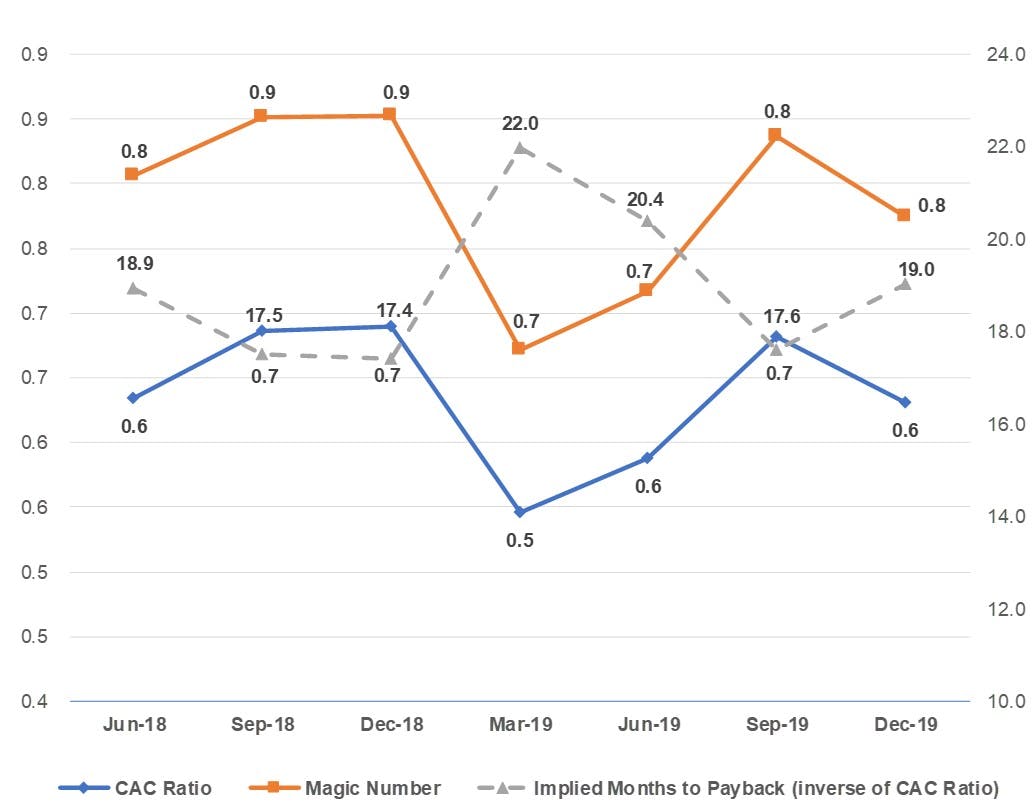

Procore is quite a bit larger than the 2019 cohort of SaaS IPOs and is growing fast with no signs of slowing down -- they grew revenue ~55% YoY for 3 quarters straight. They also have nice expansion characteristics and were at a 117% net dollar retention rate in 2019, although that's down slightly from previous years. They're growing fairly efficiently as well; their implied months to pay back, which is the inverse of a CAC ratio (implied net new ARR multiplied by gross margin/sales and marketing spend of the prior quarter), was at a 19-month median over the past 7 quarters.

Moreover, the company raised $490M to date and has $121.8M in cash and cash equivalents on the balance sheet today. Given they reported $92.2M in a tender offer and spent $60M+ in cash on acquisitions, it implies they have spent ~$215M to get to $340M of implied ending ARR, a 1.6x ratio of implied ending ARR / implied burn at IPO. Given 1:1 is a strong ratio for a SaaS company, Procore has been quite efficient. Outputs of other metrics are below:

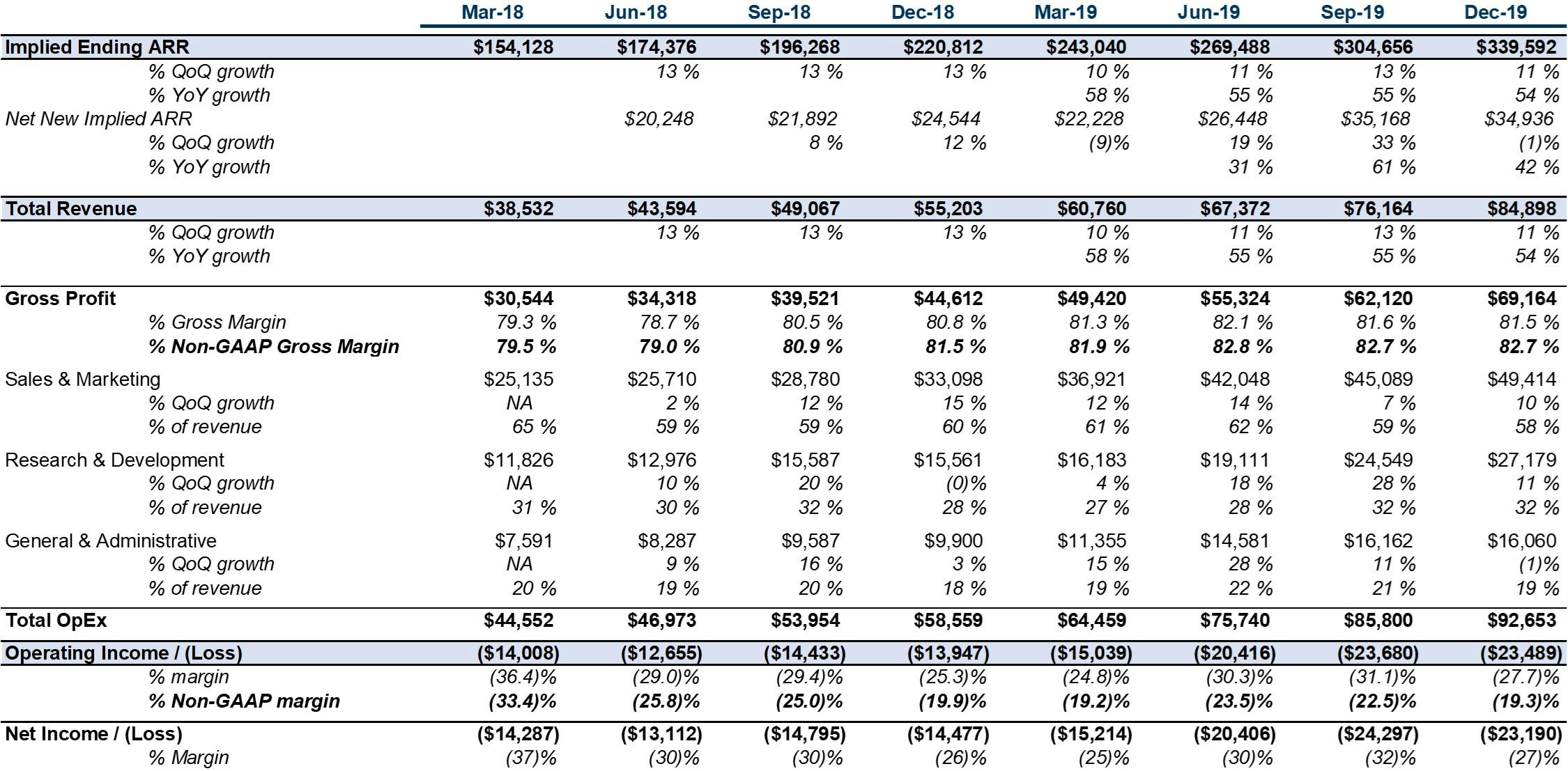

Historical P&L & Metrics ($000's)

Source: Company S-1

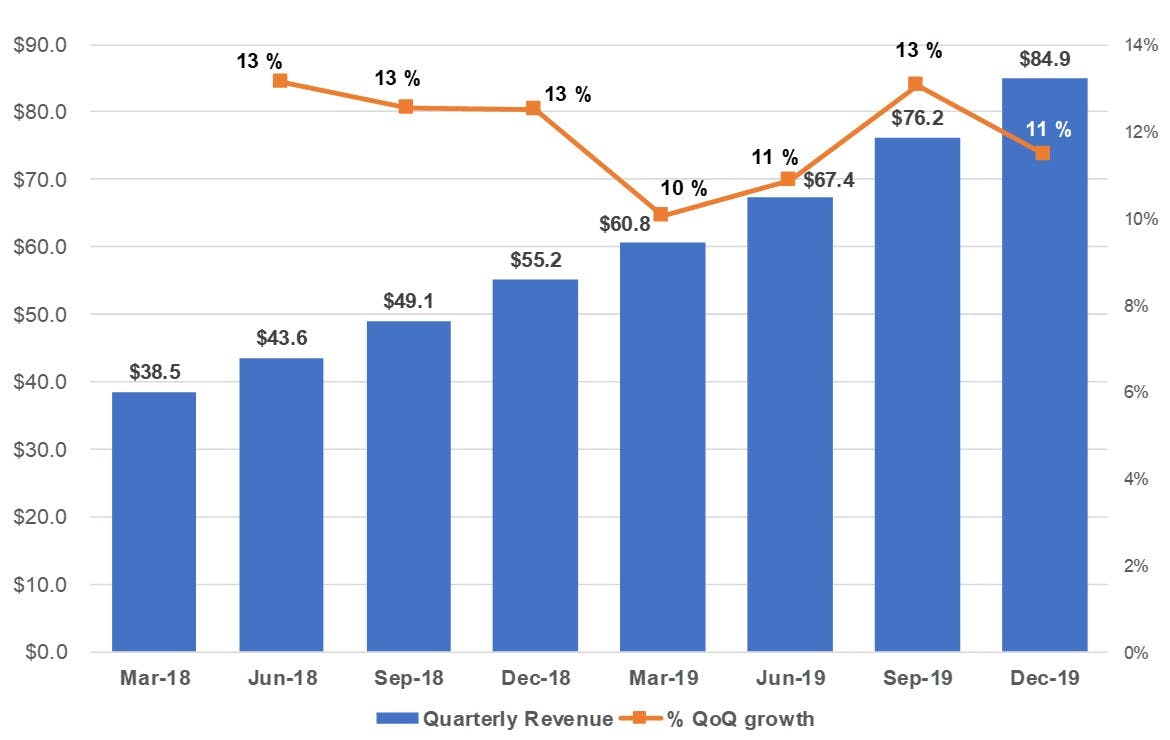

Quarterly Revenue ($M)

Source: Company S-1

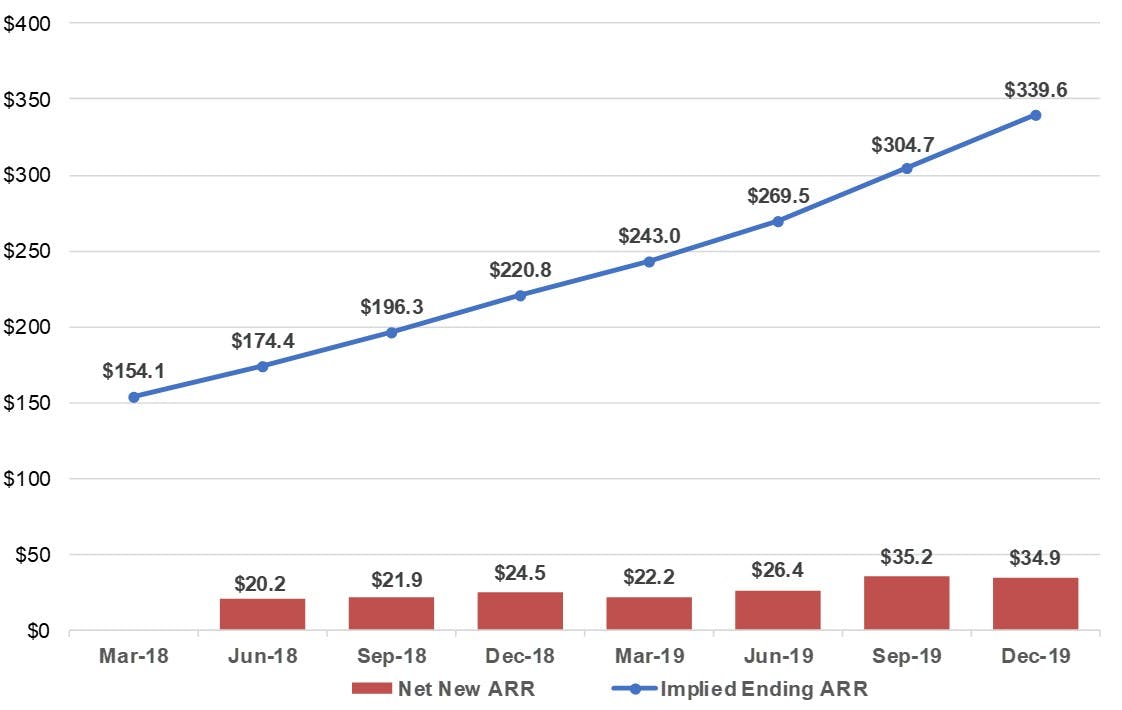

Implied Ending ARR ($M)

Procore added $34.9M of implied net new ARR over the past quarter and $118.8M over the past year.

Source: Company S-1

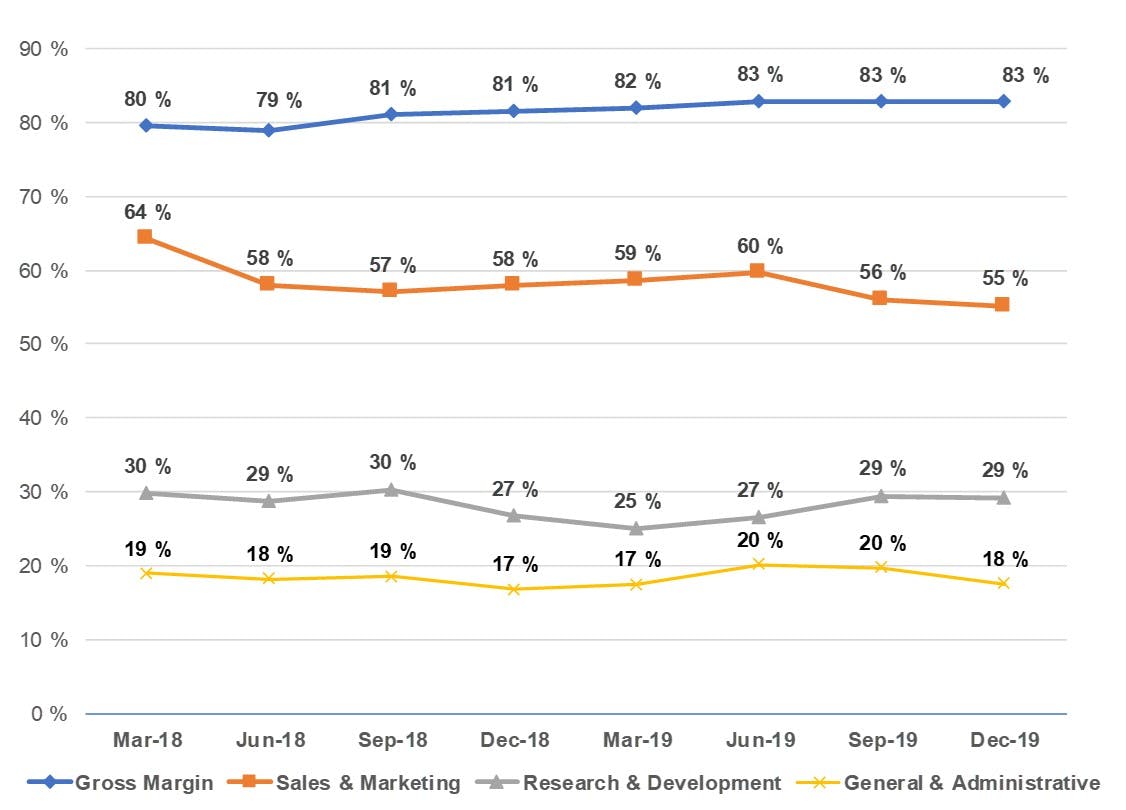

Quarterly Non-GAAP Gross Margin and Operating Expenses as a % of Revenue

Source: Company S-1

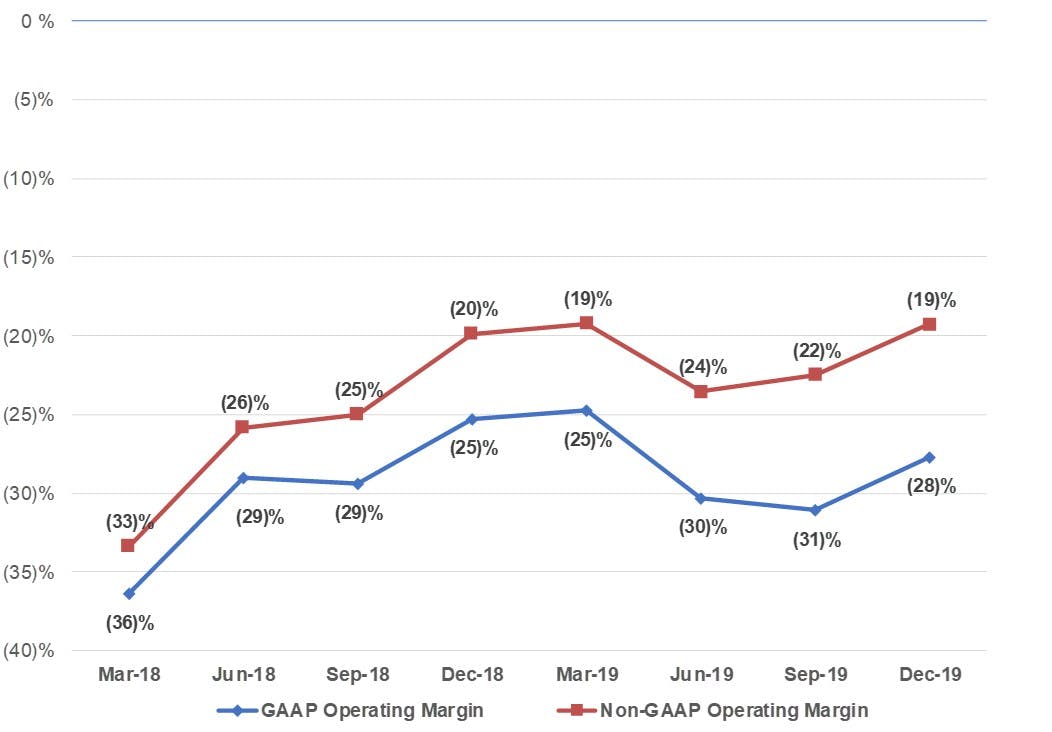

Quarterly GAAP and Non-GAAP Operating Margins

Source: Company S-1

Net and Gross Dollar Retention Rates

Procore does not release a cohort figure over time but they do release annual net and gross dollar retention rates (below).

Source: Company S-1

Sales Efficiency and Payback Periods

Procore doesn’t release customer counts by quarter, but the below output plots their implied months to payback using the inverse of a CAC ratio (net new ARR multiplied by gross margin/sales and marketing spend of the prior quarter). The magic number is defined as net new ARR/sales and marketing spend of the prior quarter. For their scale, their sales efficiency is strong. The median months-to-pay-back over the disclosure period is 18.9 months.

Source: Company S-1

Cash Flows ($M)

Source: Company S-1

Quarterly P&L (000's)

Source: Company S-1

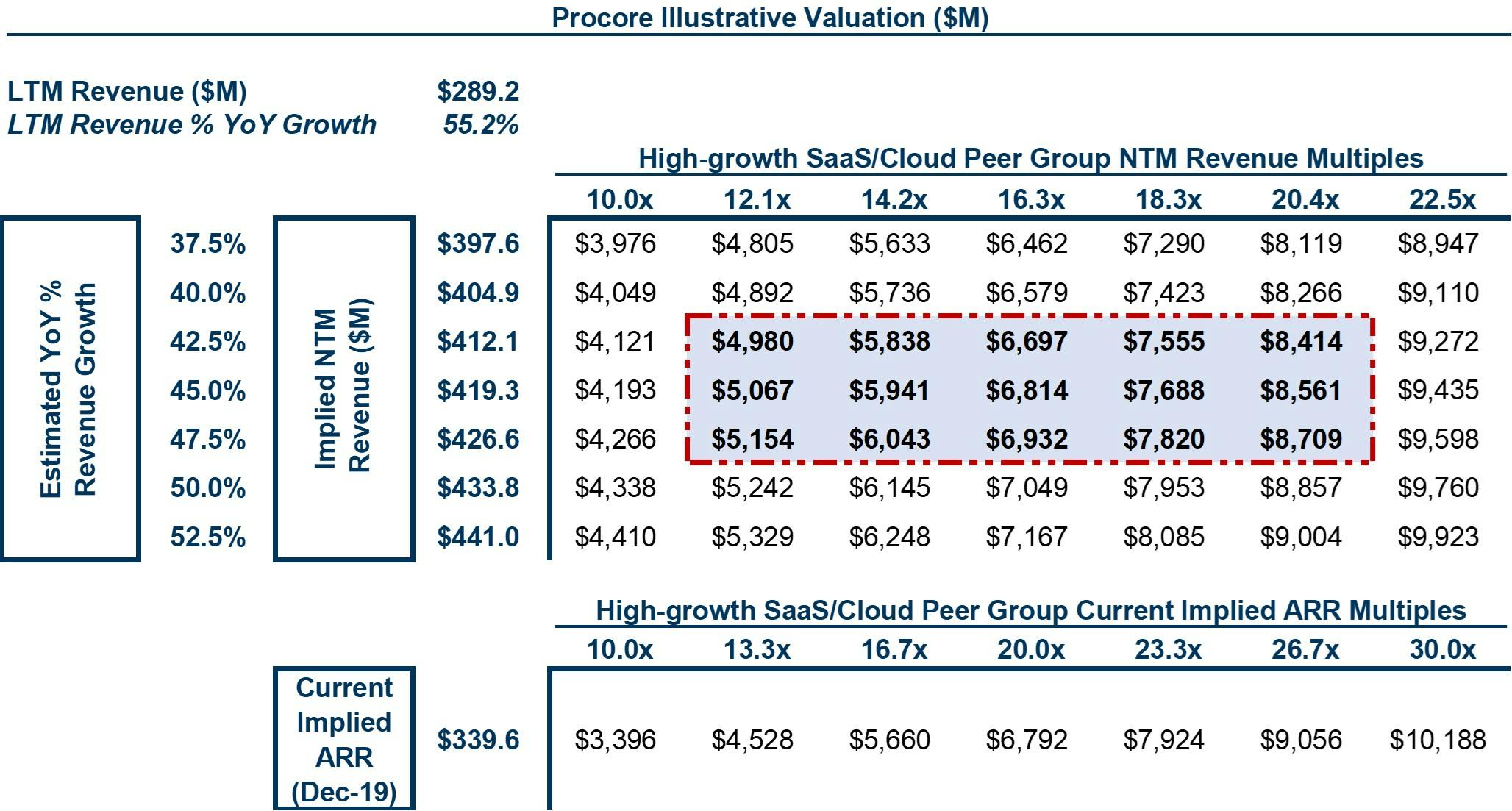

Valuation ($M)

Procore will trade like other high-growth SaaS companies: on a multiple of forward revenue. The output below uses NTM (next-twelve-months) revenue based on an illustrative range of growth rates and comparable EV (enterprise value) / NTM revenue multiples from other public, high-growth SaaS businesses. It also includes an implied ARR multiple range. As mentioned in other posts, companies do not release projections or guidance in S-1's. While the markets have come down significantly over the past week, multiples for high-growth public SaaS companies are still healthy and I suspect Procore trades above the last round preferred price of ~$4B.

Note: Enterprise value ranges and growth rates are illustrative.

Procore is one of the more impressive vertical SaaS companies to file an S-1. Software is permeating every business workflow inside an enterprise and the construction industry is no different. Procore even mentions in their S-1 "in short, we build software that helps build the world". While the industry is still lacking in its adoption of software, the market is massive and Procore is the leading, independent cloud-based player. Moreover, just over 10% of revenue is from international customers which represents a huge growth opportunity for the business. Public market investors will likely dig in on Procore's pricing model. In the risk factors the company also calls this out; if overall construction volume were to decrease customers would pay less for the software since it's generally priced on construction volume of customers. Given the recent market disruption due to coronavirus (which they also call out as risk factor), investors could fear softness in the new construction market, which is a part of Procore's business. With that said, based on a review of the S-1, Procore may be the most exciting vertical-specific SaaS company to file since Veeva did so in 2013, which has had an incredible run. It wouldn't be surprising to see Procore follow their path.

To receive these posts by email, click here.